The difference between retiring comfortably and constantly worrying.

For most individuals approaching retirement, the main question is not “How much money do I have?” The more important question is “Will my money last as long as I do?” With longer life expectancies, rising healthcare costs, unpredictable markets, and evolving tax laws, retirees today face a complex financial landscape.

A sustainable retirement income plan is intended to provide clarity and peace of mind. Having a plan can help ensure you are able to maintain your lifestyle, navigate uncertainty, and enjoy the retirement you’ve worked hard to build.

Understanding YOUR Retirement Needs

Creating a reliable income stream begins with knowing how much you’ll need to support your lifestyle. This is why, at Comprehensive Wealth Management, everything starts with our planning process. A comprehensive financial plan includes many factors such as longevity, inflation, healthcare costs, and taxes. A successful plan accounts not only for current needs but for how those needs may change over time. There is no one-size-fits-all scenario, so we work with clients to create a plan that is tailor-made to their unique needs and situation.

The Three Pillars of Retirement Income

Most retirees draw income from a combination of sources. Understanding how these are utilized over time is integral to the success of any plan.

Guaranteed Income. These are sources that provide stable, predictable payments; such as Social Security, pensions, and guaranteed annuity payments. Guaranteed income forms the foundation of retirement cash flow as these are funds that can be counted on throughout retirement.

Part-Time Work or Alternative Income. Some retirees chose to bridge their early retirement years with part-time or seasonal work, consulting in their respective field, or income from a rental property. While not required, supplemental income can significantly reduce pressure on your investment portfolio during the early years of retirement.

Investment Withdrawals. Your retirement accounts (IRAs, ROTH IRAs, taxable brokerage accounts) supply supplemental income needed to support your lifestyle.

Tax Efficiency Considerations (aka The Tax Control Triangle)

Taxes can be one of the most overlooked and largest expenses in retirement. A sustainable plan carefully orchestrates withdrawals from different account types: taxable, tax-deferred, and tax-free. A coordinated strategy blends these accounts to manage tax brackets, avoid IRMAA surcharges, and reduce RMD burdens - optimizing the Tax Control Triangle and working to extend portfolio life.

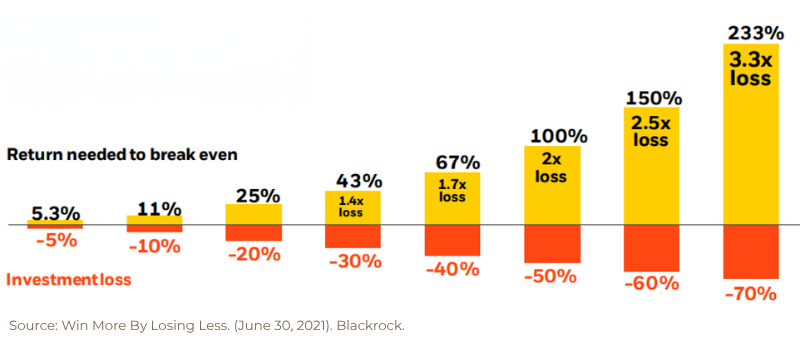

Managing Market Risk

The danger of market downturns early in retirement, when withdrawals are often highest, is a real concern for new retirees. As the chart below highlights, the sequence of returns greatly impacts what your portfolio needs to earn after a down market to get you to break even. To mitigate the risk of a market downturn, a sustainable plan often includes a diversified portfolio that is regularly rebalanced. At CWM, one of the ways we diversify portfolios is by blending strategies to help manage risk and achieve your goals.

Social Security Optimization

Social Security is often the largest guaranteed income source in retirement. The decision of when to claim, between ages 62 and 70, can drastically impact your total lifetime benefits. As with most things in life, there is no “best” option that works for everyone.

There are multiple factors to consider such as health, spousal benefits, working situation, and spending expectations early in retirement. I often find myself answering clients’ questions with “It depends”. Determining when to take Social Security is possibly one of the biggest times that answer applies. Having a comprehensive financial plan is the only way to truly answer what timeframe makes the most sense.

Planning for Healthcare and Long-Term Care Costs

Healthcare is one of the biggest variables in retirement, and ignoring it can threaten even the strongest plan. In particular, long-term care is commonly underestimated in terms of cost. Considering healthcare coverage options, including Medicare, are vitally important to any plan and discussions about long-term care costs, such as insurance, self-funding, or family help need to happen WELL in advance of retirement. Custodial care costs, in particular, need to be thought about when you are relatively young (around age 50) and insurable. This gives you runway to analyze the best way to cover this need. While Medicare Part B and D are generally simple to forecast, out of pocket costs often exceed expectations, especially in your elder years.

Reviewing and Updating the Plan Annually

A retirement income plan, just like a full financial plan, is not a one-time document. It is a living strategy that needs to adapt and be updated as your life evolves. We review withdrawal rates at every meeting to make sure the current plan is sustainable. Discussing and documenting any life changes helps ensure that investment risk still aligns with your stated goals and timeline. The only constant in life is change and thus any plan needs to be able to change as well.

* * * * * * *

A sustainable retirement income plan provides more than numbers. It provides confidence and peace of mind. By integrating all these steps, you can build a retirement that is both financially secure and helps you live richly.

Whether you’re a decade away from retirement or already in it, now is the time to ensure your income strategy is built on a solid foundation. At CWM, we have 25 years of experience working with clients to help them live richly in retirement. Contact us or call the office at (425) 778-6160 to schedule a complimentary 30-minute call with a CWM advisor for a second opinion on your current financial situation.

As a financial planner with CWM, Jason works closely with our clients to ensure their needs are met and exceeded. Jason is a capable and seasoned problem-solver, providing service on a variety of complex topics while keeping client's end goals in mind.

From complimentary, no-pressure initial consultations to ongoing client strategy meetings, CWM financial advisors are here to explore your goals and create a road map to help you live richly.

Schedule a complimentary, no-pressure phone call with a CWM financial advisor to learn if our breadth of consulting services and purpose-driven approach aligns with your needs.